F&I pros who don’t include a completed Accept/Decline form in every deal jacket are not only failing to capitalize on a proven sales tool, they’re putting their dealerships at risk.

by Joe Porter

September 6, 2018

5 min to read

The old “Accept/Decline” form — you need to have it in every deal, right? In my travels to dealerships where I assist in deal audits, it’s surprising how many deal jackets are missing this important document. Some explanations for missing the form include:

“The customer bought everything. Why bother?”

“That was an employee deal.”

“No one told me I had to.”

Ad Loading...

Another common occurrence is an incomplete form in the deal jacket. It may be unsigned or only have the customer’s name on it. Common responses include:

“Hey, I make sure there’s one in every deal with the customer’s name on it. That’s all that’s important.”

“They are a repeat customer and they never buy anything.”

“It’s part of my recap.”

Let’s examine each of these “explanations” to understand the peril we could be putting the dealership in.

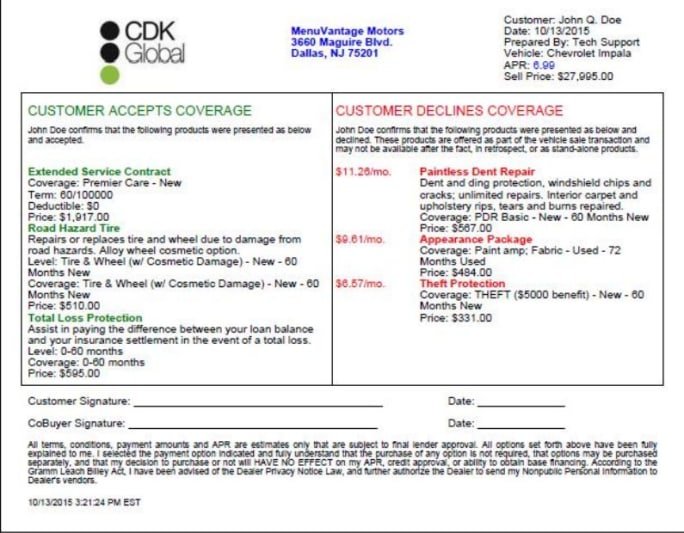

“The customer bought everything. Why bother?” Have you ever had a customer who came back a few days after delivery saying that unauthorized products were added into his or her payment? The customer makes a big scene and demands to see the manager, who will fix the problem and fire you.

If you don’t have the technology to record every deal in the business office, then the Accept/Decline form is the next best thing. There is no better feeling than pulling the deal out and showing the customer the Accept/Decline form he or she signed — by hand — agreeing to the products purchased with the full understanding that purchasing them was not a condition of taking delivery. Disaster avoided.

Ad Loading...

“That was an employee deal.” We sometimes sell vehicles to employees that do not need the vehicle as much as we need the unit at closeout. We take for granted that they will be grateful for the below invoice pricing they received and will sign away with 100% faith that we are doing it the right way.

But most employees eventually become former employees. And when employees leave the dealership, they usually call to cancel the products to ease the burden on their budget from their unexpected new car payment. When they find out that canceling the products will not lower their payment, just their payoff, they get a sudden urge to threaten the dealership with lawsuits and media attention about rumors of payment packing. In this case, simply faxing their attorney a copy of the completed Accept/Decline form with all signatures matching would help things return to normal very quickly.

“No one told me I had to.”

This could unfortunately be true. This is a conversation to have with your current product provider on why your F&I associates are not up to speed on why this form is such a critical piece of a paper or digital trail to demonstrate compliance should your store be visited by a regulator or plaintiff’s attorney.

However, I usually find out that this same F&I manager has four out of 10 deals with Accept/Decline forms in them. So this person could be suffering from a memory issue or all this producer needs is a simple reminder to fill this form out with every customer. This is where a deal checklist can help.

Ad Loading...

“Hey, I make sure there’s one in every deal with the customer’s name on it. That’s all that’s important.” This is a very dangerous position to be in. What if the customer or a concerned family member comes to see you to arbitrate what the buyer purchased? A form with just the customer’s name on it would be like bringing a slingshot to a gunfight.

“They are a repeat customer and they never buy anything.” This is similar to the scenario where the customer buys everything. I have also seen too many instances where the repeat customer doesn’t buy anything. You then determine it is a waste of time to have the Accept/Decline form filled out because the customer said: “I’ll take my chances.”

Then it happens: The customer’s car gets totaled or needs a new transmission to the tune of $2,000. Now the customer wants the dealership to cover the repair because you never offered GAP or a service contract. If you would have offered the product, the customer would have bought it. Unlikely story. However, without the Accept/Decline form, you cannot prove anything to the contrary, so the dealership may be faced with undue exposure.

Nowadays, some stores will let you keep your job if you agree to the payroll deductions to cover the mistake and any future claims. This is not a good option.

Concerned yet? Good.

Ad Loading...

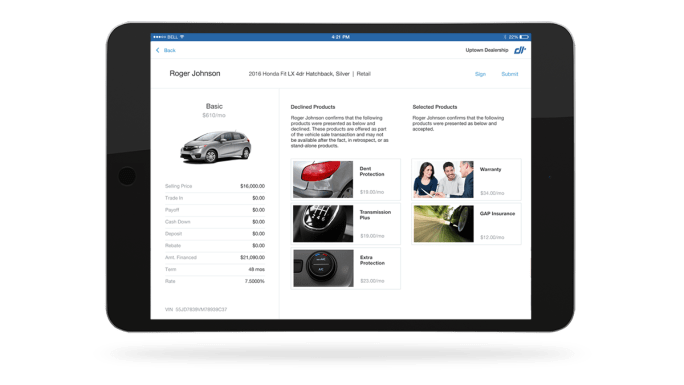

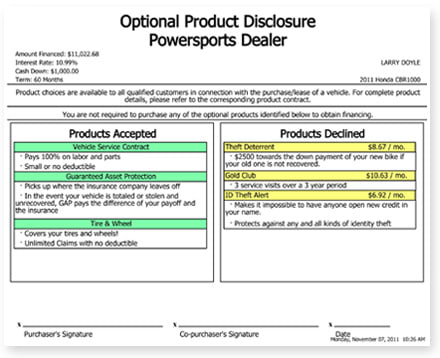

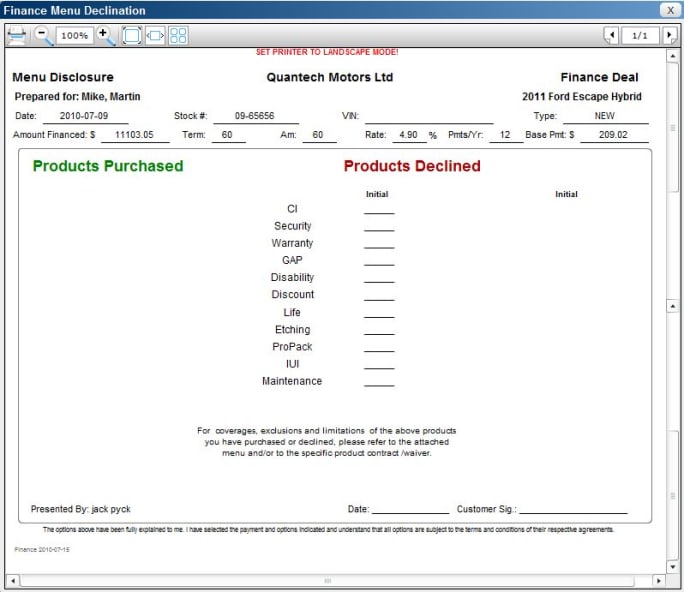

Now let’s look at how the Accept/Decline form can make you money. Sometimes, when you present an effective menu customized to the buyer’s needs, the customer declines the suggested products for miscellaneous reasons. With an Accept/Decline form, the consumer is instructed to initial by each service being declined and to review his or her responsibility should an event occur.

This will help illustrate that by purchasing the product, the customer could save money should he or she have a claim. Reading this might persuade the customer to take a second look at certain products and ask for options to add it with minimal pain to the budget. Extending the term or working more cash down will serve everyone in the long run.

A completed Accept/Decline form is critical to every deal. This simple form will protect you and the dealership from financial harm and professional embarrassment. Who knows? It may even inspire your next customer to take a second look at that one product he or she knows makes sense and ask you to help find a way to fit it into his or her budget. In so many ways, the Accept/Decline form truly can be an F&I manager’s best friend.

Joe Porter is a trainer with American Financial & Automotive Services Inc. Email him at joe.porter@bobit.com.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.

A TransUnion study found that relationship-driven sales models proved to be important, as consumers who used an agent had a lower shopping intensity than those going it alone.

In this video, Reese Dailey of the Automotive Training Academy by Assurant reveals strategies to make cash deals profitable without relying on monthly payment bumps.

Suite of new APIs, product enhancements and integrations is designed to help maximize contracting and funding efficiency for lenders and their dealer partners.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.

In this video, Reese Dailey of the Automotive Training Academy by Assurant explains how to handle a customer who isn’t willing to listen to your pitch.

Third-quarter battery electric vehicle insurance claims were up 4% year-over-year. A new report says EV claims cost the most due to complex technology and limited after-market parts supply.