CHICAGO — The overall consumer credit market is projected to remain on a healthy trajectory in 2018, but the expected growth in credit balances should be viewed as a reflection of consumer sentiment toward the economy than an indicator of consumers struggling to keep up with their obligations, TransUnion said this week.

The year should also see auto loan balances continue to grow, albeit at a slower pace, and serious delinquencies sticking with their upward trend. TransUnion also expects the shift to used-vehicle financing on the part of prime customers to continue, although it also believes hurricanes Harvey and Irma will provide a temporary boost in demand for new vehicles to open the year.

“TransUnion anticipates many shifts in the auto loan market during the course of 2018,” said Brian Landau, senior vice president of auto finance for TransUnion. “While the growth in loan balances is likely to continue to slow in 2018, we may see some exceptions to that trend, especially in early 2018. The impact of the hurricanes in Florida and Texas will likely result in up to 900,000 replacement vehicles being purchased, which would impact both total balances and debt per borrower in the early part of 2018.”

In the long term, however, the firm expects the shift to used-vehicle sales to offset some of the waning demand for new vehicles, which should also impact overall balances as well as average amounts financed. TransUnion expects the later to grow at a slower rate, as finance sources are expected to require larger down payments to meet certain underwriting requirements (e.g., lower loan-to-value ratios and shorter terms).

“This is also being impacted because of less equity in vehicles in which consumers are trading back,” the firm noted.

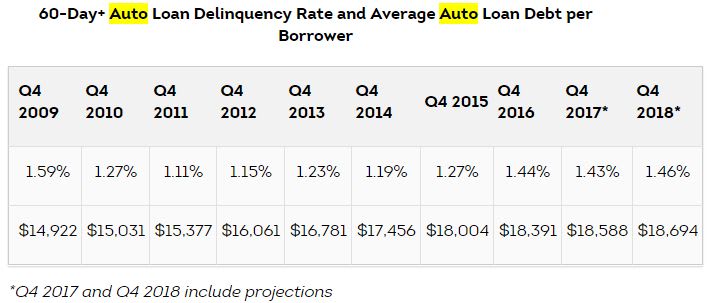

Landau also believes serious delinquencies, or loans more than 60 days past due, will fall nearly 20 basis points by the mid-point of 2018 before ending the year three basis points higher than where he expects them to be by the end of 2017. “As in recent years, we should see the usual seasonal shifts in serious delinquency rates,” he noted, adding that the delinquencies should still end the year below peak levels recorded during the Great Recession.

The rise in delinquencies is also expected by finance sources, which Landau said will continue to steer their respective portfolios “in a fashion that suggest they are still cautiously taking on some rick.” It’s that pullback, which he said began in the third quarter, that has led to a share shift in favor of the prime plus and superprime segments by 2.3 percentage points.

“We expect this trend to continue in 2018,” the firm noted in its report. “The shift in lending toward lower risk consumers will help cushion the market over the next few quarters.”