TransUnion: Auto Finance Registers Lowest Growth Rate Since Q1 2012

The firm attributed the slowdown to improvements in oil states and tightening underwriting guidelines, which have also helped stabilize delinquency rates.

by Staff

May 14, 2018

2 min to read

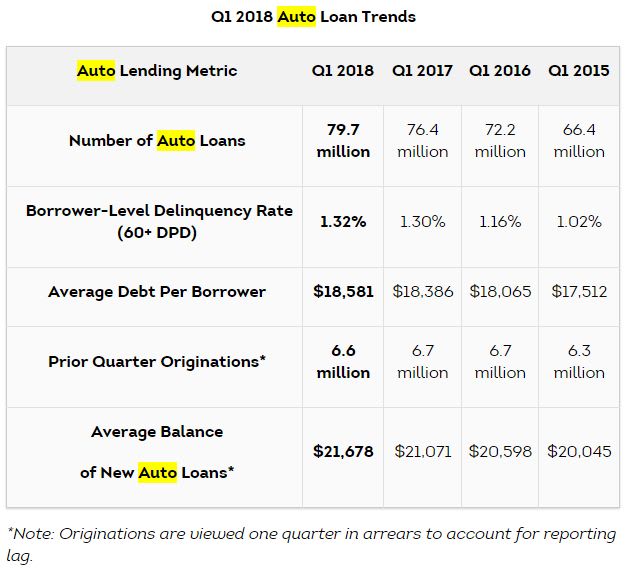

CHICAGO — Tighter underwriting guidelines and better on-time payment in oil states had a positive effect on serious auto delinquency rates per borrower, according to TransUnion.

After growing 1.16% in the first quarter of 2015 to 130% in last year’s opening quarter, the serious delinquency rate — or loans more than 60 days delinquent — stayed relatively flat at 1.32% in the first quarter 2018.

Ad Loading...

“The first quarter of 2018 was relatively quiet in the auto finance space,” said Brian Landau, senior vice president and automotive business leader at TransUnion. “The most noteworthy change was the stabilization in the delinquency rate, likely due to shifts in the makeup of new auto loan borrowers and continued improvements in oil states.

“Gas prices, as measured by WTI crude, have increased more than 21% in the last year, which has provided a significant boost to the local economies of oil-producing states.”

The top six states with the largest annual decreases in delinquency rates in Q1 2018 — Alaska, Wyoming, Texas, New Mexico, Oklahoma, and North Dakota — are among the eight states where oil, gas, and mining account for 10% or more of gross domestic product. The other two states — Louisiana and West Virginia — also performed better than the national average in terms of annual changes in their serious delinquency rates, according to TransUnion.

The firm also observed a continued shift in the origination makeup of auto loan borrowers, as finance sources continued to migrate to higher credit tiers. This led to the lowest annual growth rate in auto loan balances since the first quarter of 2012. They rose 5.2% to $1.183 trillion.

Overall originations, viewed on quarter in arrears to account for reporting lag, declined 1.5% in the fourth quarter of 2017 — the sixth consecutive quarter of year declines, though the smallest such decrease in 2017.

Ad Loading...

“Origination mix continues to shift toward lower risk, with superprime and prime plus taking 1.8 points of share from prime, nearprime, and subprime on an annual basis,” Landau said. “This continues the trend from last year, where the shift to the two lowest risk tiers was 1.6 points.

“Finally, we believe the slowdown in auto loan balance growth is largely due to the decline in originations, as lenders continue to tighten their underwriting requirements and rising interest rates put a slight damper on demand.”

In this video, Reese Dailey explains how effective follow-up drives better results

across the dealership, including increased sales, higher F&I penetration, and

stronger customer retention.

It may be human nature to back off when a customer seems to say no to a product or service. But experts say F&I managers should operate as though the answer will be the opposite.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.

A TransUnion study found that relationship-driven sales models proved to be important, as consumers who used an agent had a lower shopping intensity than those going it alone.

In this video, Reese Dailey of the Automotive Training Academy by Assurant reveals strategies to make cash deals profitable without relying on monthly payment bumps.