NEW YORK — Concerns about a subprime auto finance crisis are no more, at least according to the S&P/Experian Consumer Credit Default Indices. It showed that default rates for auto loans have drifted down in the last four months, but not all consumer credit categories were a picture of health in May.

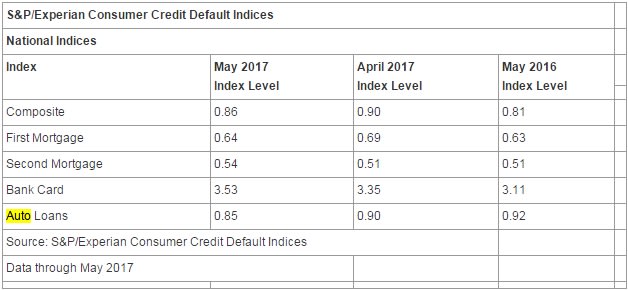

The composite rate for consumer credit defaults dropped four basis points from April to 0.86%. By segment, auto loan and first mortgage defaults decreased five basis points each from April to 0.85% and 0.64%, respectively. The bank card default rate, however, increased 13 basis points from April to 3.53% — a 48-month high.

"The pictures of auto loans and mortgages are quite different,” said David M. Blitzer, managing director and chairman of the Index Committee at S&P Dow Jones Indices. “At the beginning of the year there were reports of a sub-prime crisis in auto loans; these concerns seem to be behind us. The first mortgage default rate remains at 1%, lower than the pre-crisis period. Rising home prices and increases in the equity mortgage borrowers have in their home are helping lower default rates.”

Blitzer noted that one factor playing into rising bank card defaults and stable defaults on mortgages and autos are interest rates: about 4% on mortgages and 4.4% on auto loans, compared to 12%-18% on bank card loans.

He added that in the past, default rates began to climb around the same time the growth of bank card credit outstanding began to slow. He noted that year-over-year growth of bank card credit outstanding peaked at 6.8% last November and was at 5.7% in April, the latest figure available. Bank card defaults rose from 2.81% in November to 3.35% in April, and up to 3.53% in May.

When comparing the bank card default rate among the four census divisions, the default rate in the South is considerably higher than the other three census divisions. The East South Central Census Region — comprised of Kentucky, Tennessee, Alabama, and Mississippi — has the highest bank card default rate. As per the Bureau of Labor Statistics, these states have some of the lowest median household income.

"Easy come, easy go: bank cards, where borrowing money requires simply swiping a credit card, are experiencing rising defaults, while defaults on other kinds of consumer credit, which depend on paperwork, are flat or down," said David M. Blitzer, managing director and chairman of the Index Committee at S&P Dow Jones Indices. "Default rates on bank cards are at the highest level since May 2013.”

Overall, four of the five major cities saw their default rates decrease in the month of May. New York experienced the largest decrease, down nine basis points from April to 1.01%. Los Angeles reported a default rate of 0.66% for May, dropping three basis points from the previous month. Dallas came in at 0.67%, down two basis points from April. Miami was down one basis point from April to 1.29%. At 0.97%, Chicago was the only city reporting a default rate increase of three basis points from the previous month.

Jointly developed by S&P Dow Jones Indices and Experian, the S&P/Experian Consumer Credit Default Indices represent a comprehensive measure of changes in consumer credit defaults. They track the default experience of consumer balances in four key loan categories: auto, bankcard, first mortgage lien, and second mortgage lien. For more, visit www.consumercreditindices.standardandpoors.com.