DETROIT — The new-vehicle sales pace is expected to be the lowest for the month of May since 2013, according to a joint forecast from J.D. Power and LMC Automotive. And with the slowdown expected to continue in the second half of the year, LMC reduced its retail light-vehicle sales forecast for the year to 13.9 million.

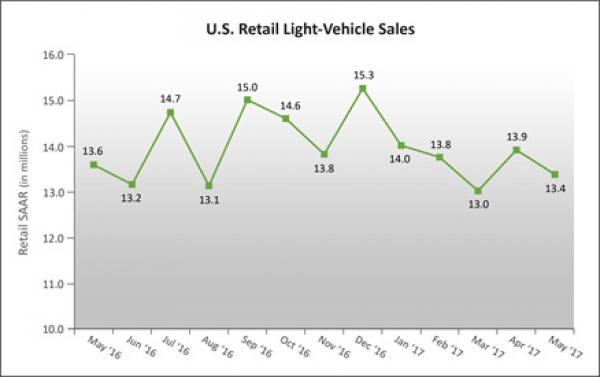

Even with an additional selling day this year, May retail sales are expected to fall 2.9% from a year ago to 1.22 million units. May’s seasonally adjusted annualized rate (SAAR) for retail sales is expected to come in at 13.4 million units, a 212,000-unit decrease from a year ago.

Not even record incentive spending for the month was expected to keep sales on pace with a year ago, with spending per unit through the first 11 days of the month rising by $241 from a year ago to $3,583 per unit. Incentives as a percentage of MSRP stood at 9.9%, putting them on pace to exceed the 10% level for 10th time in the past 11 months.

Despite maintaining record incentive levels, the average days to turn for the industry is above 70 days for the first time since 2009. More than 27% of vehicles sold so far in May sat on dealer lots for more than 90 days, up from 25% last year.

“Continued elevated incentives reflect the challenges of balancing record levels of inventory and are likely to remain elevated unless production is adjusted to meet consumer demand,” said Deirdre Borrego, senior vice president of automotive data and analytics at J.D. Power.

Last week, the two firms put the average new-vehicle retail transaction price for the month at a record $31,419. The previous high of $30,886 was set last May. And with record transaction prices, consumers are on pace to spend $38.4 billion on new vehicles in May, about $1 billion more than last year’s level and a record for the month.

Incentive spending on trucks and SUVs stood at $3,358 when the two firm issued their projections last week. That’s up $187 from last year. Incentive spending on cars stood at $3,942, up $344 from a year ago.

As of May 25, trucks accounted for 61.7% of new-vehicle retail sales — the highest level ever for the month of May and the 11th consecutive month above 60%.

Days to turn, or the average number of days a new vehicle sit on a dealer lot before being sold to a retail customer, reached 71 through May 14. This is the highest level for any month since July 2009 (80), according to the two firms.

Fleet sales are expected to total 320,300 units in May, down 5.8% from May 2016 on a selling day-adjusted basis. Fleet volume is expected to account for 20.8% of total light-vehicle sales, a decrease from 21.3% in May 2016.

“On the surface, continued downward pressure on auto sales since the beginning of the year is troubling. However, we believe some of the weakness year to date has been exaggerated by jitters over policy risk with the Trump administration,” said Jeff Schuster, senior vice president of forecasting at LMC Automotive. “If uncertainty dissipates and tax cuts are initiated — or OEMs engage higher incentives — stronger demand could return for an encore performance in the second half of the year. However, the industry still must deal with negative effect of a growing used-car market and the notion of rising interest rates, both of which are real risks to future volume and potential growth.”

Based on reassessment of market indicators and uncertainty risk, LMC cut its forecast for 2017 total light-vehicle sales from 17.5 million units to 17.2 million. This would represent 2% sales decline from 2016. The firm also cut its retail light-vehicle outlook from 14.2 million units to 13.9 million units, which would represent a 1.4% sales decline from 2016 if realized. The reduction in fleet volume has outpaced that of retail, with fleet volume expected to be down 4.5% from 2016.