The average household is on the verge of being priced out of the new-vehicle market, Experian’s fourth quarter data shows.

by Melinda Zabritski

April 10, 2017

4 min to read

The auto finance industry broke several records in the fourth quarter of 2016. Not only did total open loan balances rise by $987 billion from the prior-year period to a record $1.072 trillion, amounts financed for both new and used reached new highs in 2016’s end-of-year quarter.

A major driver was the 3.1% year-over-year increase in new-vehicle sales in December, which was more than enough to push the industry’s annual sales tally above the 17.5 million-unit mark last year. The concern, however, is whether the average household is being priced out of the new-vehicle market.

Ad Loading...

On the new side, the average amount financed reached a record $30,621, while the average for used rose from $18,850 in the year-ago quarter to a new high of $19,329. That’s a $11,292 gap between the cost of new and used vehicles — the highest my firm has ever observed. Here’s a look at some of the trends that shaped the auto finance industry in 2016’s end-of-year quarter.

Priced Out

With the upward trend in new and used finance amounts, many consumers are turning to alternative methods like extending terms, attaining short-term leases or opting for a used vehicle to keep payments affordable. But as previously mentioned, the average American household may not be able to afford a new car in this environment.

In fact, the percentage of consumers opting for longer auto loan terms continues to grow. In the fourth quarter, the percentage of consumers who selected 73- to 84-month loan terms for their new-vehicle purchase increased from 29% in the prior-year period to 32.1%, while the percentage of used-vehicle buyers who opted for terms in the 73- to 84-month term band increased from 16.4% in the year-ago period to 18.2%.

While these lower monthly payments help consumers stay within their monthly budgets, the trend comes with some serious implications. The biggest is negative equity, as these lower monthly payments won’t keep up with depreciation. This puts consumers in a situation where they are trading in a car that’s upside down a few years down the road. And the expected increase in interest rates will exacerbate the situation, as car buyers will pay more in interest since they have stretched their payments.

Ad Loading...

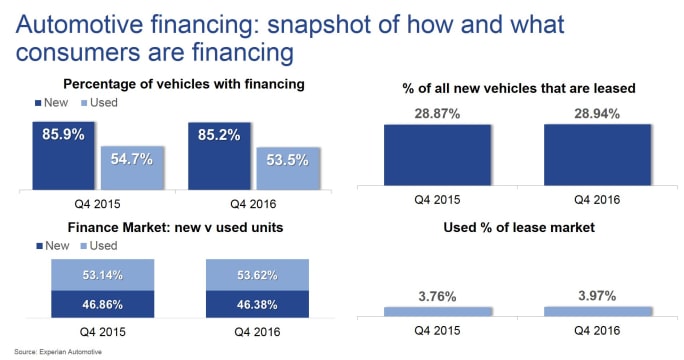

Leasing also continues to be a popular option for payment-conscience consumers. In the fourth quarter, the average lease payment was $92 less than the average monthly payment for a new financed vehicle. While the overall leasing percentage has fallen slightly from the 30% range observed in the first half of 2016, it remained high at 28.94% in the fourth quarter.

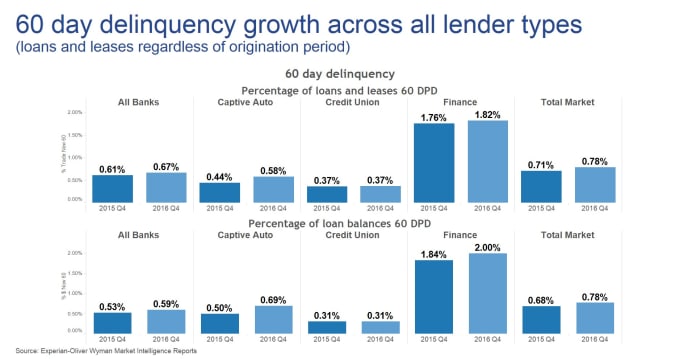

Cause for Concern Most consumers are still making timely payments, but delinquencies registered a larger year-over-year increase than in the past. While 30-day delinquencies increased slightly from 2.42% in the year-ago period to 2.44% , 60-day delinquencies experienced a more significant increase in the fourth quarter. They rose from 0.71% in the year-ago period to 0.78%.

The rise in delinquencies came primarily from customers of captive finance companies, with the segment’s 30-day delinquency rate jumping from 2.23% to 2.32%. The segment’s 60-day delinquency rate also jumped from 0.44% to 0.58%.

But as delinquencies rose last year, finance sources responded by shifting their originations toward customers with better credit. For new-vehicle loans, the average credit score rose from 712 in the year-ago quarter to 714. For used, the average credit score jumped five points from a year ago to 654.

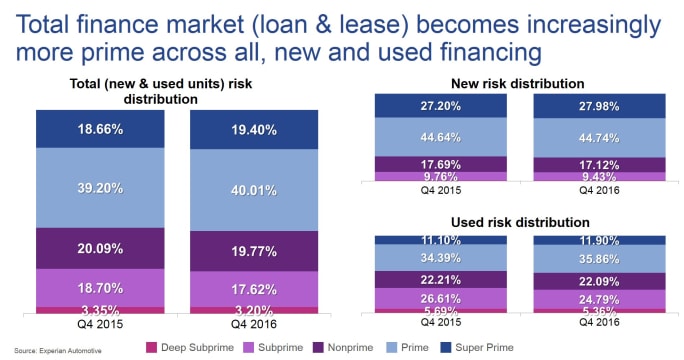

In fact, the share of deep-subprime and subprime financing decreased from 22.05% in the year-ago period to 20.82%, while the share of prime and superprime financing jumped from 57.86% to 59.41%. These trends should influence delinquency rates positively in the future.

Ad Loading...

A shift toward higher credit was also observed on the used side. In the fourth quarter, used-vehicle financing in the superprime risk tier grew 5.4% from a year ago to 41.85%. Moreover, used franchise and independent vehicle dealers registered the biggest year-over-year gains in superprime financing, with growth of 5.91% and 13.8%, respectively. Much of these increases are due to more prime consumers choosing to finance used vehicles instead of new.

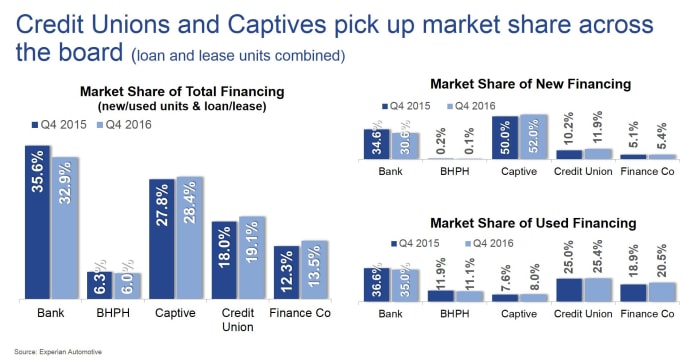

Finance Companies, Credit Unions, Captives Gain Market Share In terms of overall market share, credit unions and captive finance companies continued to gain market share in the end-of-year quarter, while banks pulled back in both new and used financing. Finance companies registered the largest percentage growth in total vehicle financing, with the segment’s share growing from 12.3% in the prior-year period to 13.5%. Credit unions and captives also increased their share of total vehicle financing, growing from 18% to 19.1% and from 27.8% to 28.4%, respectively.

Banks saw their share drop from 35.6% in the year-ago quarter to 32.9%. For new vehicles, the segment’s share fell from 34.6% to 30.6%. Banks fared slightly better in the used-vehicle market, with their share inching down from 36.6% to 35%. Buy-here, pay-here financing also lost ground, with the segment’s share dropping slightly from 6.3% in the year-ago period to 6%.

Overall, the auto finance market has continued a run of solid performance. Increases in delinquency rates are a concern, but decreases in high-risk loans signal a positive lending response to help mitigate these issues. Affordability continues to be a concern, as rising finance amounts begin to price more consumers out of the new-vehicle market.

Melinda Zabritski serves as senior director of automotive credit for Experian Automotive. Email her at melinda.zabritski@bobit.com.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.