The auto finance market continued to drive forward in the fourth quarter of 2010, but can it continue? Experian Automotive’s director of automotive credit runs through the numbers.

by Melinda Zabritski

April 4, 2011

5 min to read

Driven by further declines in 30- and 60-day delinquencies, the auto finance market continued to stabilize in the end-of-year quarter of 2010. And with consumers continuing to improve their repayment patterns, lenders made it clear they’re ready to loosen up their lending standards.

Illustrating the more aggressive posture on the part of lenders was the increase in the share of loans made to credit-challenged customers. The market, however, remains more conservative than what was seen in 2007 and 2008; nevertheless, it’s clear lenders are feeling a lot better these days.

Ad Loading...

The following analysis will provide a snapshot of consumer activity during fourth quarter of 2010, as well as a comparison with the prior year.

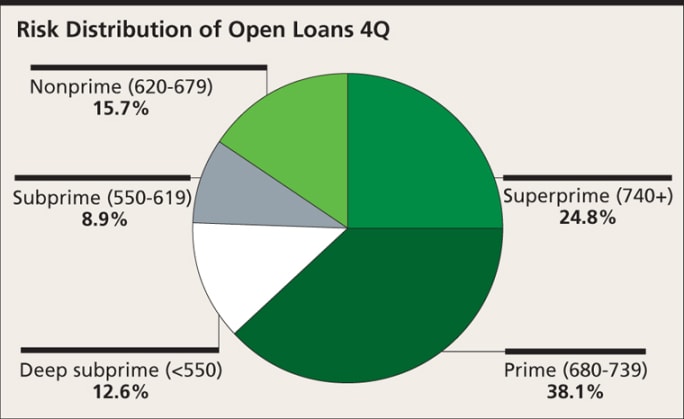

Risk Distribution Reveals Conservative Posturing

A key indicator of the overall health of the automotive finance market is the distribution of risk among all open loans. And as a reminder, Experian Automotive uses five risk segments to classify consumer loans: superprime (740+), prime (680–739), nonprime (620–679), subprime (550–619) and deep subprime (<550).

Over the last several years, the low-risk prime and superprime segments have garnered the majority of automotive loans, and that remained the case in the fourth quarter. During that period, the two segments accounted for 62.9 percent of all open automotive loans, up from 60.8 percent in the fourth quarter of 2009.

The highest risk segment, deep subprime, experienced a significant year-over-year drop in share, falling to 12.6 percent in the fourth quarter from 15.3 percent in the year-ago period. Subprime, however, showed a slight increase, inching up to 8.9 percent from 8.8 percent in the year-ago quarter. Nonprime also showed an increase, growing from 15.2 percent in the fourth quarter of 2009 to 15.7 percent.[PAGEBREAK]

Ad Loading...

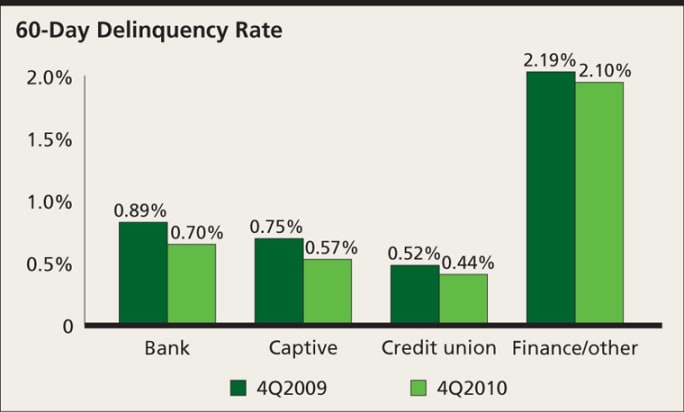

Delinquencies See Sharp Decline

For the third consecutive quarter, 30- and 60-day delinquency rates experienced year-over-year declines. Sixty-day delinquencies dropped 15.26 percent, contracting from 0.94 percent in the year-ago period to 0.79 percent in the fourth quarter of 2010.

Banks realized the largest decline in 60-day delinquencies. That group saw its rate drop 0.19 percentage points from the year-ago period to 0.70 percent in the fourth quarter of 2010. Following close behind was the captive segment, which saw its 60-day delinquency rate drop 0.18 percentage points from a year ago to 0.57 percent.

Credit unions and finance companies experienced single-digit percentage point drops, with credit unions falling 0.08 percentage points to 0.44 percent and finance companies edging down 0.09 percentage points to 2.10 percent.

Thirty-day delinquencies dropped by 9.71 percent from the year-ago period to 2.98 percent in the fourth quarter of 2010. Experiencing the biggest decline was the captive finance segment, which saw its rate drop 0.45 percentage points to 3.07 percent. Experiencing the smallest decrease was the credit union segment, which saw its 30-day rate inch down 0.10 percentage points to 1.72 percent.

Ad Loading...

[PAGEBREAK]

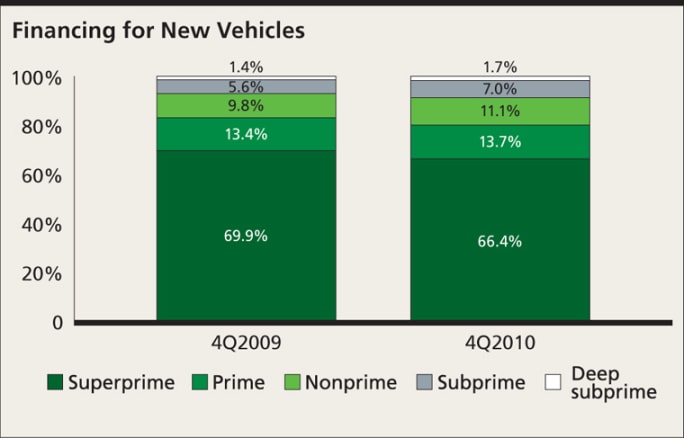

New-Vehicle Loans More Accessible to the Credit-Challenged

While overall open auto loans were relatively stable, loan originations for new vehicles revealed that lenders are getting more aggressive. The share of loans made to credit-challenged, new-vehicle customers grew by 18.2 percent in the fourth quarter compared to the year-ago period.

A breakdown of the below-prime segments showed that loans made to nonprime customers jumped from 9.75 percent in the year-ago period to 11.14 percent in the fourth quarter of 2010. New-vehicle loans made to subprime customers also experienced a year-over-year increase, with the credit tier’s share jumping from 5.6 percent to 6.96 percent. Even the deep subprime segment realized a year-over-year increase, inching up from 1.44 percent to 1.74 percent in the end-of-year quarter.

For both new and used, the share of loans made to nonprime, subprime and deep subprime customers increased from 36.42 percent in the fourth quarter of 2009 to 38.42 percent in the fourth quarter of 2010. However, those tiers still have a lot of catching up to do. In the fourth quarters of 2007 and 2008, the share of loans for credit-challenged customers stood at 44.63 percent and 41.03 percent, respectively.

Ad Loading...

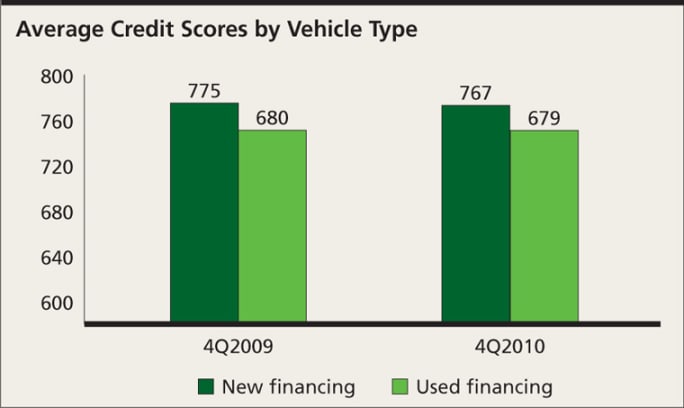

Average New-Vehicle Credit Scores Rise

Further evidence that lenders are loosening their loan criteria can be found in the average credit score for new-vehicle buyers. In the fourth quarter of 2010, the average credit score for a new-vehicle buyer dropped eight points from the year-ago period to 767. However, lenders were still far more conservative than they were in the fourth quarter of 2007, when the average credit score for new-vehicle customers stood at 749.

For used-vehicle loans, the average credit score remained nearly unchanged from the year-ago period, dropping just one point to 679 in the fourth quarter. Lenders remained relatively conservative with respect to used-vehicle loans in comparison to the fourth quarter of 2007, when the average credit score for a used-vehicle loan stood at 661.

Lenders Taking Some Risks, But Remain Cautious

With consumers doing a better job of making payments on time and lenders experiencing less volatility in their loan portfolios, the auto finance market should continue to improve. The industry is already seeing lenders loosen their guidelines for nonprime and subprime customers, which represent a significant portion of the automotive market.

Ad Loading...

Still, the market remains much more conservative than what was seen in 2007 and 2008, but it is clear lenders are becoming less risk averse. The hope now is that the auto finance industry will continue to gain momentum and help drive the auto industry toward recovery.

Melinda Zabritski serves as director of automotive credit for Experian Automotive. E-mail her at melinda.zabritski@bobit.com.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.