Not only are lenders staying away from anything subprime, they’re also pushing more consumers toward the used-vehicle market. And with more than $5.7 billion in loans reported 60 days delinquent, Experian Automotive predicts further market volatility.

by Melinda Zabritski

July 1, 2009

6 min to read

The changing market dynamics

experienced by automotive finance sources last year continued to pose

significant challenges for the automotive finance market in the first quarter

2009, with the high-risk consumer segment and delinquencies continuing to grow.

What’s clear is risk

mitigation is the name of the game in what remains an unpredictable automotive

lending market, with most traditional lenders moving away from the high-risk

credit category. That spells further problems for dealers attempting to get

credit-challenged consumers financed.

Ad Loading...

The first quarter also saw an

increase in the number of car buyers being pushed out of new-car loans and into

the used-vehicle market, another sign of the struggling economy’s influence on

lender guidelines.

This month’s quarterly

automotive finance analysis examines the challenges faced by the automotive

finance industry, and provides a snapshot into consumer activity during the

first quarter 2009.

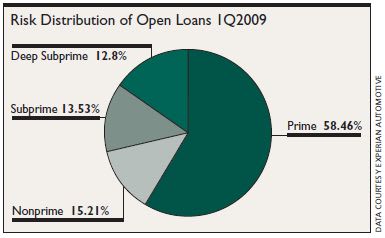

Distribution of Automotive Loans By Lending Tier

Looking at the market by

lending tier provides a clear picture of the shifts in credit quality among all

open automotive loans held by consumers across the country. And during the

first quarter, the trend of consumers shifting into lower credit tiers

continued. For instance, while more than 58 percent of consumers with

automotive loans were considered prime, the category decreased by 2.6 percent

from the first quarter 2008.

Experiencing the greatest

growth in the first quarter was the deep subprime population, which increased

6.03 percent from the prior year. This resulted in 12.8 percent of consumers

falling into this high-risk category. Also increasing were the nonprime and

subprime segments, which saw increases of 3.08 percent and 1.87 percent,

respectively.

Ad Loading...

[PAGEBREAK]

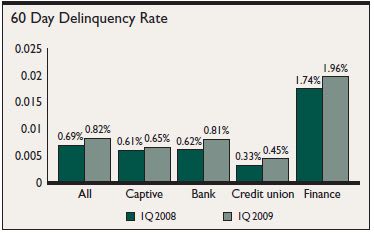

Loans 60 Days Past Due

Increases in delinquency are

one of the leading causes of consumer credit shifts, and is one of the most

significant data points on which lenders focus. As lenders experience

increasing losses due to delinquency, the availability and details of lender

programs may change, impacting the credit programs available to dealers.

As seen over the last several

quarters, the trend of increasing delinquency continued in the first quarter

2009. Loans 60 days delinquent reached 0.82 percent during the measurement

period, an increase of 19.5 percent from the prior year. Not only did the rate

of 60-day delinquency increase, but the outstanding dollar balance increased by

more than 21 percent, resulting in more than $5.7 billion in loans reported 60

days delinquent.

Credit unions, which

represent 23 percent of all open automotive loans, had the lowest rate of

60-day delinquency, yet experienced the greatest increase in delinquency rates

(36.9 percent). The segment’s lower rates of delinquency resulted in it having

the lowest at-risk balance of 60-day delinquent loans ($663 million).

Ad Loading...

Banks accounted for nearly 37

percent of all open automotive loans and had the second highest rate of 60-day

delinquency at 0.81 percent, an increase of 31.7 percent from the prior year.

Due to their high market penetration and rising delinquency rates, banks had

the greatest at-risk loan balance with more than $2 billion in automotive loans

reported 60 days delinquent.

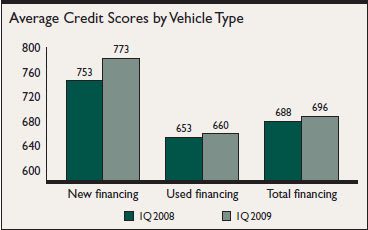

Credit Scores by Vehicle Type

The trend of tightening

credit continued in the first quarter 2009, as seen with the increase in

average credit scores for both new- and used-vehicle financing. The average

credit score for vehicles financed in the first quarter was 696, an increase of

eight points.

New-vehicle financing

experienced a 20-point increase in scores, resulting in an average credit score

of 773. Used-vehicle financing, which didn’t tighten as much as new financing,

also saw an increase of seven points resulting in an average used-vehicle score

of 696 during the quarter.

[PAGEBREAK]

Ad Loading...

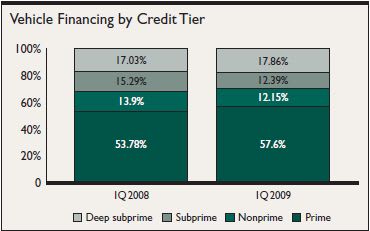

Credit Distributions by Vehicle Type

Along with higher credit

scores, the overall distribution of new-vehicle financing leaned significantly

toward consumers in the prime risk segment. However, both new- and used-vehicle

financing saw increases in the prime segment of more than 10 percent from the

prior year.

Higher risk consumers, while

still finding financing in the automotive space, had greater penetration in the

used-vehicle market. But while more than 53 percent of used-vehicle financing

was found outside of the prime market, the higher risk segments did contract

from the prior year. In fact, the most significant reduction in the

used-vehicle finance market was the subprime segment, which shrunk 17.05

percent from the previous year (new financing saw a 35.66 percent reduction).

The highest risk segment,

deep subprime, represented 20 percent of used-vehicle financing and only 1.56

percent of new-vehicle financing. The most significant reduction was seen in

new financing, with more than 48.7 percent fewer loans being financed. Used

financing, however, experienced an increase of 3.2 percent in this high-risk

category.

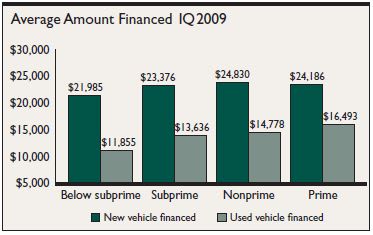

Average Amount Financed

Ad Loading...

The average amount financed

in the first quarter 2009 for new vehicles was $24,176, a decrease of $606 from

the prior year. Used-vehicle financing decreased by $1,259, bringing the

average amount financed on a used loan to $15,320.

Across the risk tiers,

new-vehicle financing varied little as credit changed. The highest amount

financed on new vehicles was seen in the nonprime population, which averaged

$24,830, a decrease of $858 from the prior year.

As credit scores changed,

used-vehicle financing experienced greater deviations. Prime consumers financed

approximately $4,638 more than below subprime consumers in the used market.

However, the used market experienced the greatest decreases in the amount

financed. The largest of these decreases was seen in the subprime segment,

which fell by $2,079. This resulted in consumers within this segment financing

on average $13,636.

[PAGEBREAK]

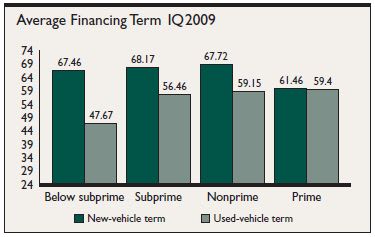

Average Term

Ad Loading...

Across all risk tiers, the

average loan term for the first quarter was 59 months. While terms vary

considerably by credit tiers, each risk group saw considerable decreases in

monthly terms — with used-vehicle financing experiencing the greatest

reductions.

The average term for

new-vehicle financing across all risk tiers was 62 months, with the longest

terms held by the higher risk loans. However, despite having longer terms,

these segments experienced the greatest term contraction for new financing.

Below subprime saw a reduction of 1.42 months, resulting in an average term of

67.46 months. Subprime new loans fell by 1.15 months, bringing the average term

to 68.17 months. Nonprime and prime loans also experienced reductions of 0.82

and one month, respectively.

The average term for

used-vehicle financing across all tiers was 57 months, with higher risk loans

experiencing the most dramatic decreases in terms. Below subprime decreased

5.83 months to an average of 47.67 months, the shortest term for used-vehicle

financing. Subprime decreased 4.47 months and nonprime experienced a 2.72-month

decrease.

Used financing for prime

consumers, while holding the longest used term (59.4 months), also saw a

decrease of 1.63 months over the prior year.

Market Unpredictability to Continue

Ad Loading...

Vehicle financing continues

to experience noticeable and notable shifts in the market. While auto loans

were originated across all risk tiers, considerable changes were made to

financing based on vehicle type. Additionally, lenders continue to tighten

their financing criteria as delinquencies increase. If the shifts outlined in

this analysis reveal anything, it’s that the changes in lending trends are

unprecedented and a bit unpredictable.

The used-vehicle market is a

good example of this volatility, as it appears to have been impacted more

dramatically by loan characteristics. In contrast, new-vehicle financing

constricted considerably, as seen with the shifts in lending to higher credit

scores.

These continued changes in

the market will present ongoing challenges for the F&I manager, as lenders

continue to evolve their finance programs based on market conditions. Having a

firm understanding of these changes will be an F&I manager’s best chance at

knowing how lenders are reacting to the market and where they need to shift

strategies to best work with lenders in their market.

Melinda Zabritski serves as the director of automotive

credit for Experian Automotive. She can be reached at melinda.zabritski@bobit.com.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.