The unusually cold weather that impacted much of the economy didn’t slow down the auto finance industry, which reached new highs in several critical metrics.

by Melinda Zabritski

April 7, 2014

4 min to read

The U.S. economy was bogged down by unusually cold weather at the close of 2013, but it wasn’t all bad news. While everyone else was sloshing through the gloom, it was all sunny skies for the auto finance industry, which reached new milestones in several critical areas.

In the fourth quarter, total outstanding loan balances, leasing and average loan amounts all reached new highs. Consumers also continued to make their payments on time, with delinquency rates falling during the end-of-year quarter. The only area of concern was the repossession rate, which showed a sizable increase from a year ago. The following is a recap of key trends from the fourth quarter 2013.

Ad Loading...

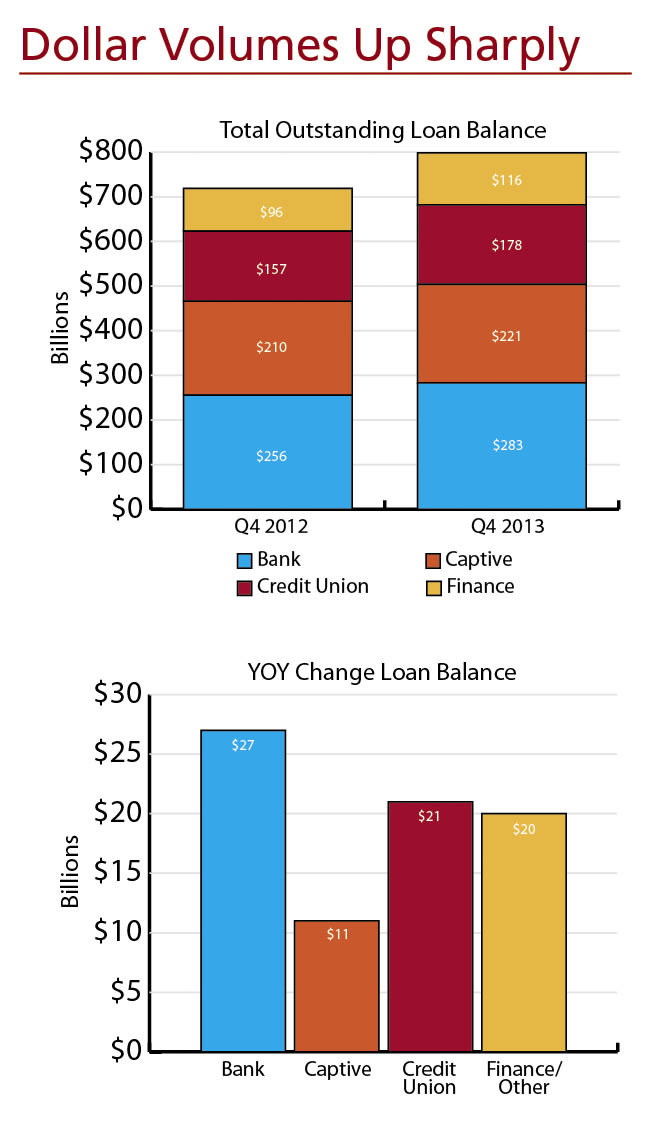

Record-High Balances Outstanding automotive loan balances jumped 11% from a year ago to $798.5 billion in the fourth quarter 2013, the highest level since Experian Automotive started publicly reporting the data in 2006. The increase in open loans spanned across all lending types, with finance companies showing the greatest year-over-year increase of 21.2%, followed by credit unions (up 13.2%), banks (up 10.5%) and captives (5.3%).

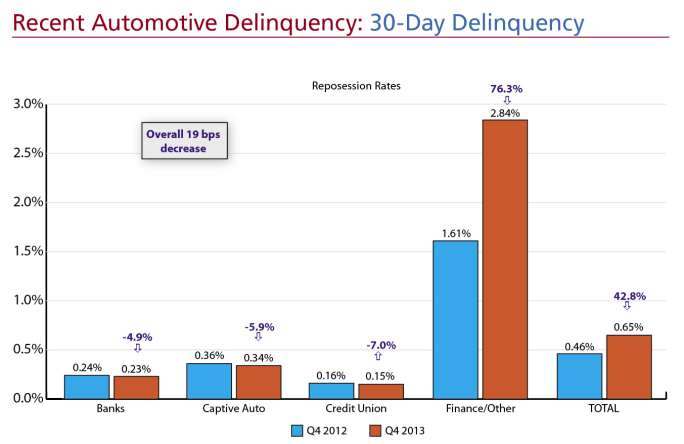

With that much money in play, it was critical that consumers make their loan payments on time. And for the most part, they did. In the fourth quarter, 30-day delinquencies dropped 3.5% from a year ago to 2.63%, while 60-day delinquencies remained flat at 0.74%.

There was one dark cloud on the horizon. Repossessions were up 42.8% in fourth quarter, rising from 0.46% in the year-ago quarter to 0.65% of all open automotive loans. However, the increase was driven entirely by finance companies, which were more active during the quarter and tend to operate in the high-risk credit segments. For that segment, the repossession rate jumped from 1.61% in the year-ago period to 2.84%.

Repossessions, however, fell for all other segments, with the rate for banks falling from 0.24% in the fourth quarter 2012 to 0.23%. For captives, the rate fell from 0.36% to 0.34%, while the rate for credit unions inched down from 0.16% in the year-ago quarter to 0.15%.

Leasing Reaches New Heights Leasing continued to be a popular option for today’s payment-conscience consumers. The transaction type, which accounted for a record 28.4% of all new vehicles financed during the quarter (up from 24.8% one year ago) was even more attractive for car buyers in the fourth quarter, with the average monthly lease payment settling in at $51 less than the average monthly loan payment. From the year-ago period, the average monthly lease payment fell from $426 to $420 in the fourth quarter 2013.

Ad Loading...

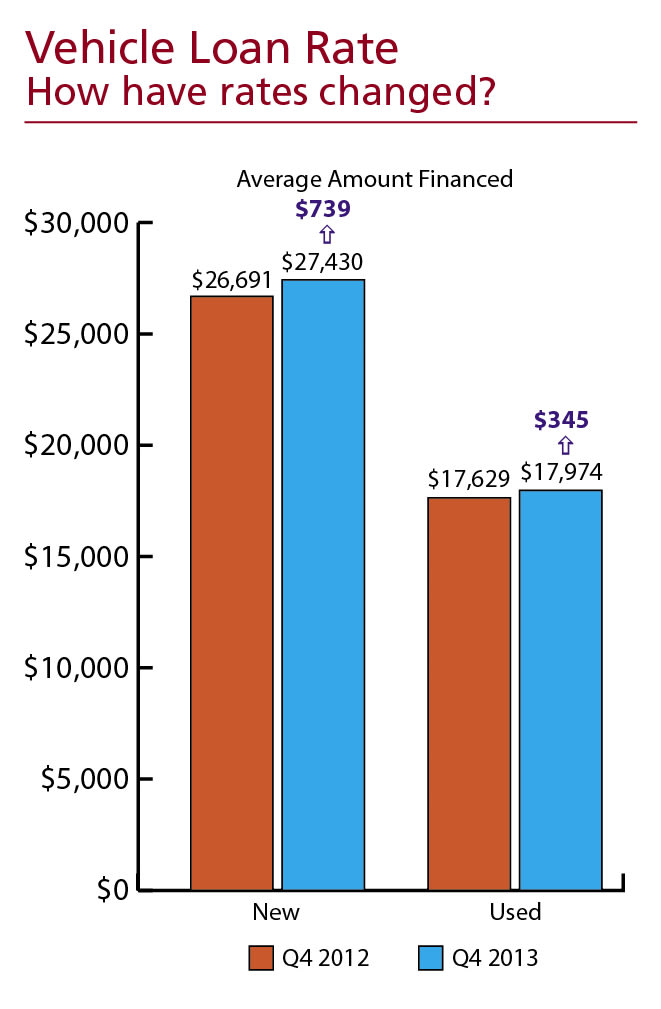

The average amount financed for a new vehicle was $27,430 in the end-of-year quarter, up from $26,691 in fourth quarter 2012. This marked the highest average loan amount for a new vehicle since 2008. It was also the first time the amount exceeded $27,000. For used vehicles, the average loan amount reached $17,974, up $345 from a year ago and the highest point since 2008.

Taking More Risks One thing a stable market does is allow finance sources to take more risks. After the recession, finance sources began employing significantly more conservative strategies. That’s changed in recent years, with finance sources increasing their risk appetite even further in the fourth quarter.

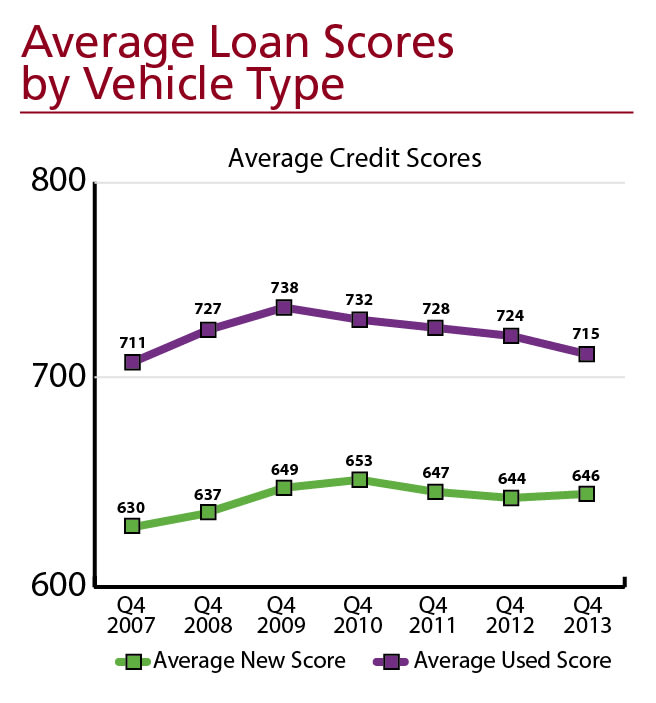

During the quarter, average credit scores for both new leases and loans decreased from the previous year. On new-vehicle leases, the average score dropped 16 points from a year ago to 719. The average score for new-vehicle loans realized a slightly smaller year-over-year decrease, dropping from 724 in the year-ago period to 715 in the end-of-year quarter.

Finance sources also increased their activity in the below-prime tiers, with the share of new-vehicle loans made to car buyers with nonprime, subprime and deep subprime credit rising from 32.8% in the year-ago period to 34.1%. For used vehicles, nonprime, subprime and deep subprime loans accounted for 62.8% of all loans, down 1.6% from 63.8% in fourth quarter 2012.

Stable Conditions The automotive finance industry remains remarkably stable despite the easing of credit standards. What that means for credit-challenged consumers who need a vehicle is they now have more financing options to choose from. Current trends also point to them being able to shop around for the best rates and terms.

Ad Loading...

But like anything weather related, conditions can change rather quickly. Much like a meteorologist monitors a barometer, executives in the automotive finance industry need to keep a close eye on how the trends fluctuate over the next few years. If things begin to sway in the opposite direction, finance sources will need to adjust their credit strategies.

Q4 2013 by the Numbers

The share of new-vehicle loans made to below-prime customers increased 3.9% from the year-ago quarter.

Average credit scores for new-vehicle loans decreased 9 points, while scores for used-vehicle loans increased 2 points.

Average loan amounts for new and used vehicles were up $739 and $345, respectively.

Loan terms on new vehicles remained flat at 65 months, while terms for used vehicles rose one month.

Melinda Zabritski serves as director of automotive credit for Experian Automotive. E-mail her at melinda.zabritski@bobit.com.

Auto loan originations rose over 6% year-over-year in the third quarter of 2025, but TransUnion predicts a slight decline in auto loan growth this year, making it an outlier in the company's overall lending forecast.

December brought some of the best borrowing availability for consumers in years, though lenders tightened their reins on riskier segments of the market.