Auto finance continues to balance the need to manage risk with the need to fuel the industry’s resurgence. So far, so good, according to Experian Automotive’s latest report.

by Melinda Zabritski

July 15, 2013

5 min to read

A quick scan of several important automotive credit metrics might bring with it a strong sense of déjà vu. Delinquencies and repossessions continued to climb, average credit scores continued to drop, finance sources continued to welcome credit-challenged customers and leasing rates reached a record high.

The good news is delinquencies and repossessions are still well below recession-level rates. The bad news is both metrics should continue to rise as more subprime auto loans coming onto the books begin to deteriorate. But as lenders have indicated to Experian Automotive, today’s subprime buyer is less delinquent than those of the past.

Ad Loading...

Lower interest rates are also working in the consumer’s favor, making vehicle payments more affordable. The 12.5 percent rise in leasing is also helping consumers ditch their aging vehicles. Overall, the auto finance market remains strong, which should continue to fuel vehicle sales as the auto industry continues down the comeback trail.

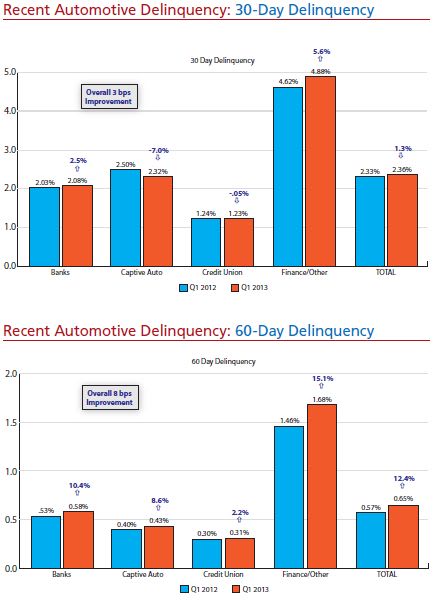

Rising Delinquencies Not a Concern

In the first quarter, 30-day auto-loan delinquencies rose from 2.33 percent in the year-ago period to 2.36 percent, while the 60-day delinquency rate increased from 0.57 percent in the first quarter of last year to 0.65 percent. Meanwhile, repossessions rose 16.9 percent from 0.43 percent in the opening quarter of 2012 to 0.5 percent this year.

It’s never good to see delinquencies or repossessions trending upward, but they are still lower than recessionary levels. Thirty-day delinquencies in the first quarter of 2008, for instance, were at 2.61 percent, while 60-day delinquencies were at 0.67 percent. Additionally, the repossession rate is still well below the peak rate seen in first quarter of 2010, when it reached 0.71 percent. The first-quarter rate is also below the 0.57 prerecession rate recorded in the opening quarter of 2008. But those pre-recession numbers should serve as cautionary benchmarks for the industry.[PAGEBREAK]

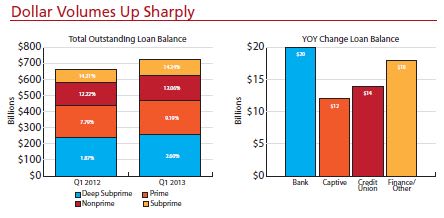

Dollar Volumes Up Sharply

Ad Loading...

One of the more telling signs of the auto finance market’s improved health is the total dollar volume of loan portfolios. And in the first quarter, that total grew by 9.6 percent from a year ago to $726 billion. Better yet, all lender types experienced growth in their automotive loan portfolios: Banks increased loan portfolios by $20 billion, finance companies by $18 billion, credit unions by $14 billion and captive finance companies by $12 billion.

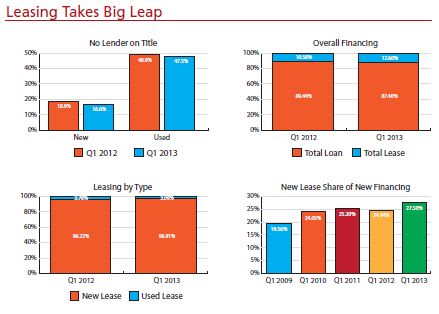

Leasing Takes a Big Leap

One of the biggest shifts during the first quarter was the increase in leasing for new and used vehicles, which jumped by 19.3 percent. Overall, leasing accounted for 12.6 percent of all vehicles financed, a 10.56 percent increase from the same period last year.

Leasing also accounted for 27.5 percent of all new vehicles financed in the opening quarter of 2013, up from 24.44 percent in the year-ago period and 19.56 percent in the first quarter 2009.

But leasing wasn’t a car buyer’s only option for keeping payments low in the first quarter. Finance sources showed they were willing to help car buyers make payments affordable by stretching out loan terms, which rose from 64 months in the year-ago period to 65 months. Interest rates were also attractive, falling from 4.6 percent in the first quarter 2012 to 4.5 percent. Both trends helped to push down the average monthly payment from $462 in the opening quarter of 2012 to $459 in the first quarter 2013.

Ad Loading...

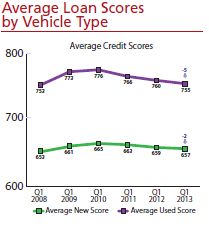

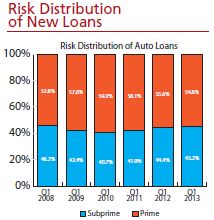

[PAGEBREAK]Below-Prime Continues to Rise

As the automotive industry has continued to improve and financial markets have stabilized, finance sources have become more willing to provide loans to consumers with lower credit scores. Overall, the average credit score for both new- and used-vehicle loans dropped compared to the opening quarter of 2012, with scores for new-vehicle loans dropping from 760 to 755. For used-vehicle loans, the average dropped from 659 in the year-ago period to 657.

Collectively, nonprime, subprime and deep subprime loans increased their share of the auto finance market to 45.2 percent, up from 44.4 percent in the first quarter 2012. For new vehicles, the share of loans made to car buyers with below-prime credit jumped to 25.1 percent from 23.16 percent in the year-ago period. For used vehicles, nonprime, subprime and deep subprime loans held 57.69 percent of finance share of the market, up from 56.77 percent in opening quarter of 2012.

The market share gains made in the below-prime spectrum helped fuel gains in market share for finance companies, which typically service credit-challenged car buyers. In the first quarter, finance companies increased their share from a year ago by 5.1 percent, capturing 15.54 percent of the market.

Banks saw their share fall by 1.7 percent to 17.25 percent of the market. Captive finance companies increased their share of the market by 3.4 percent to 17.25 percent, while credit unions captured 16.96 percent of the market, a 0.4 percent increase. Buy-here, pay-here financing had the smallest market share at 10.71 percent, down 6.4 percent from a year ago.

Ad Loading...

Keeping an Eye on Delinquencies

As stated in previous reports, the automotive credit market is healthy. However, lenders still must proceed with caution. The good news is finance sources report seeing a more responsible subprime borrower, which should help keep delinquencies in check. If that trend holds, a higher percentage of subprime loans will be a positive for the industry. After all, opening up more credit helps facilitate more sales, and that’s good for lenders and dealers alike.

Conversely, if the economy slides backward, subprime borrowers are the most likely candidates to default. In the meantime, we can sit back and enjoy the ride while keeping a watchful eye on unemployment and delinquency trends.

Q1 2013 by the Numbers

The share of new-vehicle loans made to below-prime customers increased 8.4 percent from the year-ago quarter.

Average customer credit scores for new- and used-vehicle loans fell by 5 and 2 points, respectively, from the year-ago quarter.

Leasing accounted for a record 27.5 percent of all new vehicles financed in the first quarter.

Loan terms on new vehicles rose from 64 to 65 months, while terms for used vehicles rose from 59 to 60 months.

Ad Loading...

Top 10 Auto Finance Sources by Market Share

1. Ally

6.2%

2. Toyota Financial Services

5.5%

3. Wells Fargo

5.17%

4. Chase Auto Finance

4.875

5. Ford Motor Credit

4.51%

6. American Honda Finance

4.035%

7. Nissan Motor Acceptance Corp./ Infiniti Financial Services

3.075%

8. Capital One Auto Finance

2.99%

9. Bank of America

2.13%

10. Hyundai Capital

2.09%

Melinda Zabritski serves as director of automotive credit for Experian Automotive. E-mail her at melinda.zabritski@bobit.com.

In this video, Reese Dailey explains how effective follow-up drives better results

across the dealership, including increased sales, higher F&I penetration, and

stronger customer retention.

Deal volume ebbed and flowed throughout 2025, but product performance remained steady, according to automotive technology and data intelligence solutions provider StoneEagle.

A TransUnion study found that relationship-driven sales models proved to be important, as consumers who used an agent had a lower shopping intensity than those going it alone.

In this video, Reese Dailey of the Automotive Training Academy by Assurant reveals strategies to make cash deals profitable without relying on monthly payment bumps.

Suite of new APIs, product enhancements and integrations is designed to help maximize contracting and funding efficiency for lenders and their dealer partners.