MCCLEAN, Va. — Wholesale used-car prices for vehicles up to eight years in age clawed back from February’s unexpected 1.4% drop, rebounding by 1.6%, according to the NADA Used Car Guide. While the lift wasn’t as big as the firm expected, it was in line with the period’s 2.3% average over the previous three years.

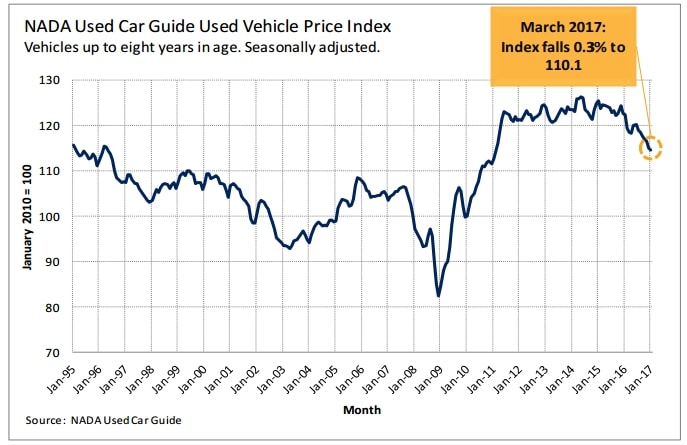

The firm’s seasonally adjusted used vehicle price index fell for ninth straight month, inching down by 0.3% from February’s 110.1 reading. Although mild, the decline put March’s index reading 7.2% below March 2016’s 118.6 reading. This marked the index’s lowest level since September 2010, according to the firm.

“March’s recovery in used-vehicle prices can be credited to typical spring season increases, which hinge largely on federal tax refunds,” NADA Used Car Guide stated in its April edition of Guidelines. “In March’s edition of Guidelines, we pointed out the negative effect of new laws involving the IRS. Essentially, the laws require the tax agency to withhold all refunds that claim the earned income tax credit and the additional child tax credit until mid-February. As a result of meeting this new process, the delay of tax refunds decreased the amount of vehicle purchases for the month, effectively depressing vehicle prices.”

The situation, however, improved in March. Per the IRS, the total number of refunds issued through March 24 was still 3.4% lower than the same period in 2016. The amount issued, however, improved by 7.6 percentage points compared to what was reported through Feb. 24. Additionally the average refund paid out through March 24 reached $2,897, which was 1.1% higher than the same period in 2016.

Prices for used mainstream vehicle segments were up across the board in March after February’s unusually soft performance. Segment level prices in March were especially strong for nonluxury small and midsize cars.

“Consumers shopping for vehicles in these segments were finally armed with fresh disposable income thanks to their recently acquired tax refunds, which logically played a role in increasing used-vehicle demand over the month,” the NADA Used Car Guide stated in its report.

After declining by 2.1% in February, subcompact car prices rebounded by 3.4% in March — the most of any segment for the month. Prices for compact and mid-size cars, however, trailed further behind, but both segments registered 2.6% increases.

Matching the industry average, mid-size van prices grew by 1.6%, followed closely by the large car segment’s 1.5% increase. Remaining non-luxury segment prices increased between 0.6% (large pickup) to 1.4% (mid-size utility). Large utility vehicle prices were flat for the month.

“Luxury vehicles fared far worse in March than their nonluxury counterparts. As a result, four out of six luxury segments experienced price losses for the period,” the firm noted in its report. “Declines were the most severe for luxury large utility and luxury large cars. Prices for the two fell by 1.5% and 1.4%, respectively.

“Meanwhile, luxury compact and luxury mid-size utility prices ticked up by 0.2% and 0.3%, respectively,” the firm added. “Overall, luxury segment losses were more severe than what has occurred during March over the past few years.”

For the month of April, the NADA Used Car Guide predicts that prices for vehicles up to eight years in age will decline by approximately 1%. Mainstream car depreciation should be less than last year, as the segment makes up for February’s depressed result. SUV and truck depreciation should be slightly worse due to ongoing increases in supply, while premium segment losses are forecasted to average less than 1% — which is an approximate 0.5-point improvement from April 2016.

“Looking out further, prices are expected to fall by about 2% in both May and June before prices deteriorate slightly more in the summer and early fall months,” the firm noted. “The overall 2017CY forecast remains unchanged. Prices are still expected to decline by about 6% in 2017, which is two points worse than 2016’s 4% loss.”