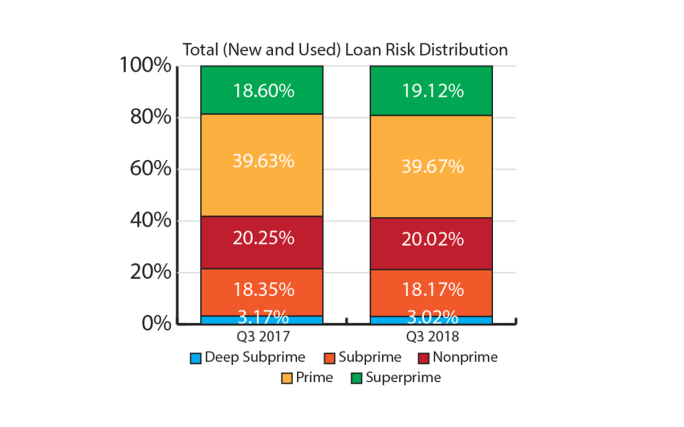

The total outstanding automotive loan balance again reached new heights in Q3 2018, hitting a record $1.17 trillion. But while the balance continued its upward trend, the mix of car buyers shifted substantially during the quarter. With many finance sources reassessing their risk-management practices and an improvement in consumer credit behavior, the percentage of subprime auto loans plunged to its lowest level in 11 years.

Subprime and deep subprime auto loans accounted for 21.19% of the total auto loan market, down 1.5% from a year ago. Alternatively, loans to prime and superprime customers rose from 58.23% in Q3 2017 to 58.79% in Q3 2018.

Much of the decrease in subprime lending was driven by higher growth rates of lower-risk car buyers in the used-vehicle market. In fact, more than 50% of the used market is made up of prime and superprime borrowers for the first time since Q3 2010.

On the flip side, loans for subprime borrowers made up the lowest percentage (22.86%) of the used-vehicle loan market on record, while used-vehicle loans for deep-subprime borrowers reached an all-time low of 4.33%.

Monthly Payments Reach Record Highs

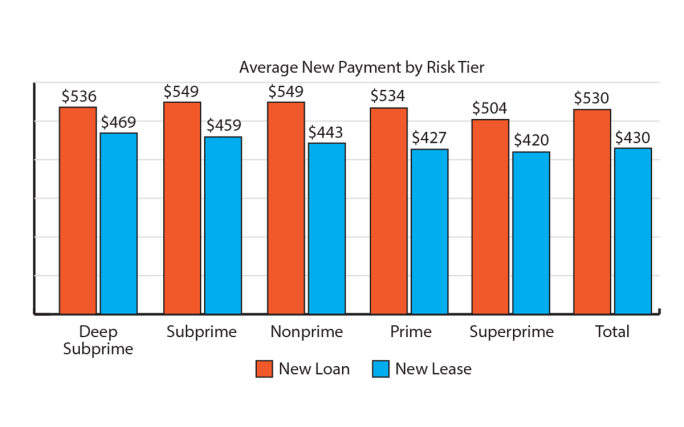

One of the trends that may be pushing many of the prime and superprime borrowers into the used-vehicle market is affordability. New and used-vehicle monthly loan payments reached historic levels as interest rates continued to rise in the third quarter of 2018. The average new-vehicle monthly payment reached $530, up 6% from a year ago. The average new-vehicle monthly lease payment was $430, approximately a 4% increase from last year. Additionally, the average used-car monthly loan payment hit a high of $381, another 4% increase.

The gap between new and used monthly payments also continues to widen, with the average new-vehicle monthly payment $149 more than the average monthly payment for used vehicles.

Given many car shoppers base their decision on monthly payment — and with such a sizeable difference between new and used monthly payments — some consumers may opt for the less-expensive vehicle.

Credit Scores and Credit Unions on the Rise

The average credit scores for new- and used-vehicle loans continued to increase, reaching 717 for new vehicles and 661 for used. Average credit scores for new-vehicle leases rose three points to 724 while new-vehicle loans also were up one point to 714. Franchise used scores increased one point to 683 while the independent space rose three points to 623.

The shifts in portfolio management have positively impacted credit unions, while banks were the only source to see a decrease in total outstanding automotive loan balances. Banks saw a decrease of approximately $1 billion in balances from a year ago, reaching $369 billion. Meanwhile, credit union balances maintained double-digit growth.

Other notable loan balance growth for this period includes captives (up 2.75%) and finance companies (up 5.07%).

30-Day Delinquency Rates Improve

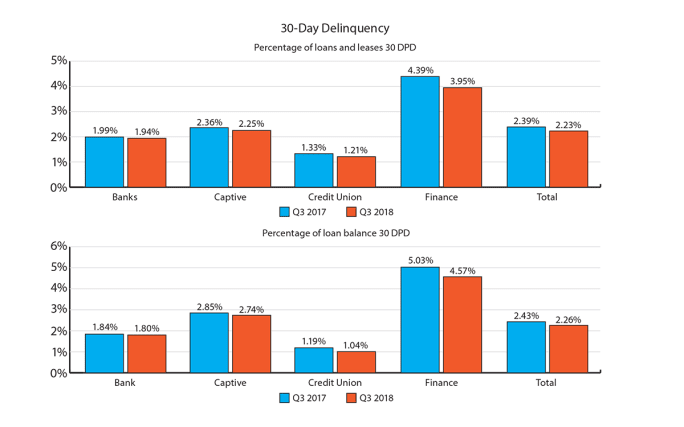

Overall delinquency rates continued to improve, providing another sign of auto loan market stability. The 30-day delinquency rate fell from 2.39% in Q3 2017 to 2.23% in Q3 2018. For 60-day delinquencies, rates fell from 0.76% in Q3 2017 to 0.72% in Q3 2018.

While the automotive finance market is cyclical, there are many factors that can contribute to shifts in market share, including consumer behavior and vehicle affordability. It’s important for auto finance sources to keep a close eye on these trends to make the right decisions and help car shoppers find affordable vehicles with the most appropriate terms — while positively impacting their portfolios.

Melinda Zabritski serves as senior director of automotive credit for Experian Automotive. Email her at melinda.zabritski@bobit.com.